While we wait for the jury to come back in the Steven Shmuel Krawatsky trial, let’s continue examining where the funding for Krawatsky’s defamation suit against the families came from.

As was mentioned in previous coverage of this trial on the blog, there’s an open motion in limine in front of the judge as to whether or not testimony regarding the Israel Charity Fund would be allowed in front of the jury. As previously covered, the Israel Charity Fund (ICF) is a charity set up by Shira Krawatsky’s brother-in-law, Zelig Bergman. The putative purpose of the charity according to their IRS filing was to provide for needy families in Israel.

According to filings by the families against Krawatsky, however, the Israel Charity Fund was a fraudulent pass-through for money to be collected on behalf of the Krawatskys to fund them and their defamation case using tax-exempt funding. If true this would be fraud.

Obviously Krawatsky’s lawyers are trying very hard to exclude any mention of this at trial. Right now the initial phase of the trial is in the hands of the jury, but these matters must still be decided by the judge for whatever the next phase of the trial ends up being.

The families filed their response to the motion in limine. It starts by saying that at this point in the trial they obviously don’t need this for phase one, but it will absolutely become necessary if the trial moves into a defamation phase since the central claim of a defamation trial is that there was some material or reputational damage done by the defendants. It’s hard to claim you’ve been materially harmed if you have an entire fraudulent nonprofit backing you up financially. Therefore, if what the families have alleged about the ICF is true, it’s directly relevant to the question of how damaged Krawatsky was by the alleged defamation.

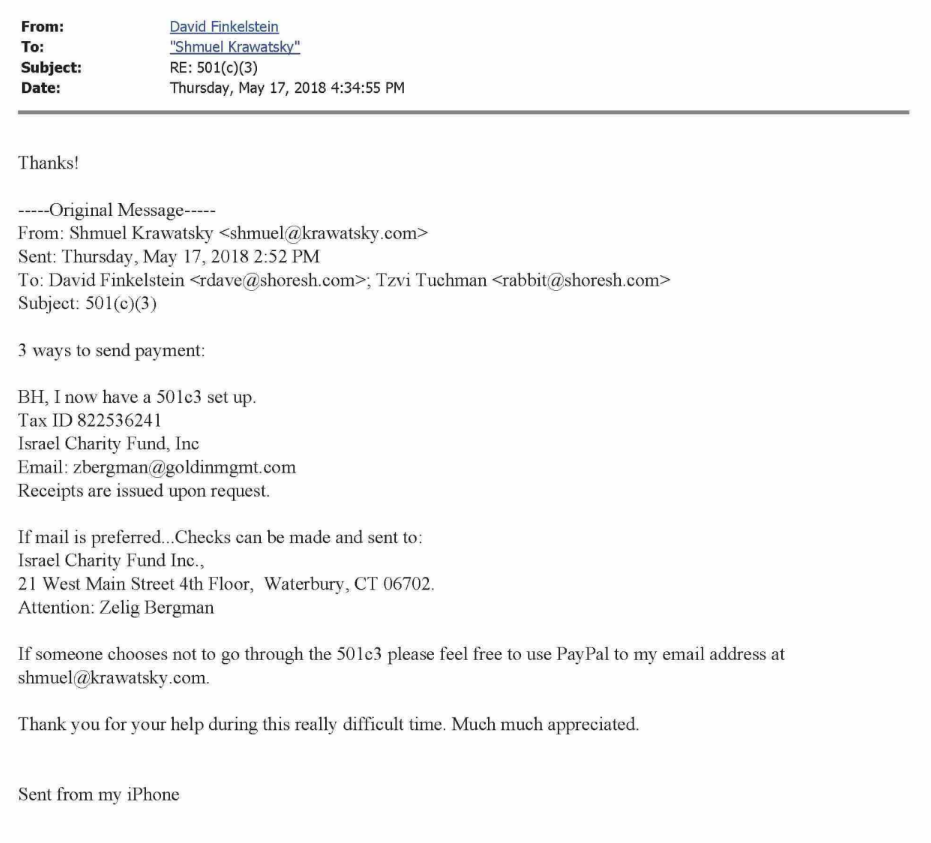

According to the motion response, the Israel Charity Fund is an organization set up by or on behalf of Shmuel Krawatsky to “help the family during this really difficult time.” The filing cites Exhibit A which is an email (screenshotted below) between Shmuel Krawatsky and Rabbi Dave Finkelstein and Rabbi Tzvi Tuchman, both of Shoresh, and dated Thursday May 17, 2018, in which Krawatsky tells Rabbi Dave that *he* now has a 501c3 set up called the Israel Charity Fund and information on how people can donate. The email also says if someone chooses not to go through the 501c3 they should feel free to use PayPal to his personal email address, shmuel@krawatsky.com. The email ends with him thanking Rabbi Dave for his help during this really difficult time, and that it was much appreciated.

Rabbi Dave answers Krawatsky thanking him.

The filing then references a second email chain between Krawatsky and Zippy Schorr, director of education at Beth Tfiloh school, informing her of three ways people can donate to the 501c3 “to help me with my overwhelming expenses.”

What’s implied in this email seems an explicit fraud. According to the mission statement filed with the IRS on the ICF’s 990, the purpose of the ICF is to “Support Jewish religious education and provide for social welfare and benefit of Jewish communities around the world.” Nowhere in that mission does it say or even imply that the money is solely for the purpose of financially supporting someone accused of raping children in launching defamation cases against his accusers.

The emails to Rabbi Dave and Zippy Schorr explicitly imply that the purpose of the nonprofit is to support the *Krawatsky’s financially* with no mention made of Jewish communities, religious education, or providing for social welfare, certainly not around the world.

The email to Schorr reiterates that if someone doesn’t want to go through the charity they should PayPal Krawatsky directly at his personal email. He then follows up with her asking when his health insurance is valid until and whether she was able to find friends to assist him with the 501c3. She answers that his health insurance is valid through August 31 and then after that he can still continue. In response to his question about the nonprofit assistance she says that she’s hoping a couple of people come through, and she wishes him a good Shabbos.

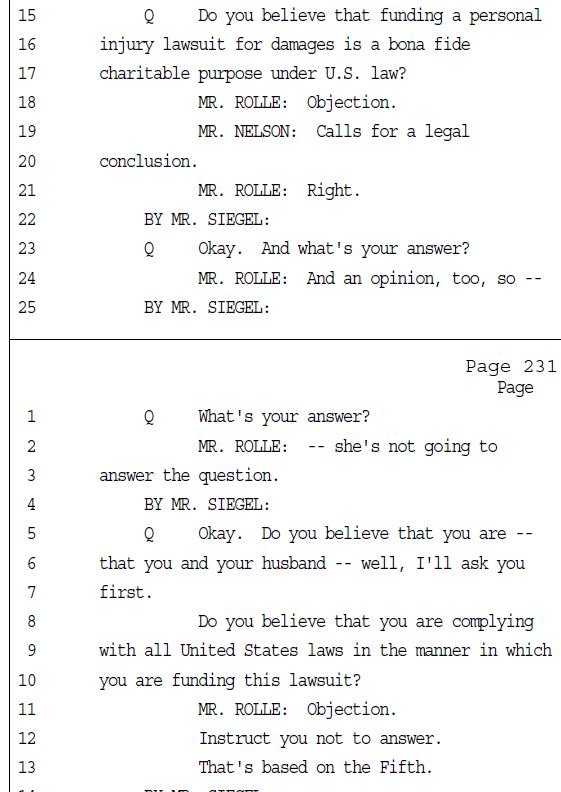

In a deposition referenced next by the filing, Shira Krawatsky is being questioned about an email sent by her husband to Rabbi Dave which says, Hi Rabbi Dave. For those who want to reach out and assist me, they may do so. To make a tax deductible donation, funds can be sent via Chase QuickPay or PayPal to Israel Charity Fund, Inc., and [an email address for Zelig Bergman]. When asked if she thought that soliciting tax-deductible donations to the Israel Charity Fund Inc. to be used to fund this lawsuit complied with U.S. law, her lawyer took the fifth on her behalf. In other words, she invoked her right not to incriminate herself. This not being a courtroom I can say that taking the fifth to that question looks pretty incriminating to me.

The filing then explains why the ICF is relevant to the case. The filing says that per an attached deposition the Krawatskys had already admitted that the ICF is relevant to the case. In particular it referenced a question asked by one of the families’ lawyers asking Shira about her sources of income, including money she received from the ICF to replace income lost as a result of the allegations, and her lawyer asks why they feel that question is relevant to the case. They answer because Shira is suing them for financial damages allegedly caused by the same allegations, and Shira’s lawyer acknowledges that that makes sense.

The filing says that the Krawatsky’s attempt to exclude any testimony about the ICF is a desperate attempt to prevent the jury from hearing that their damages are highly exaggerated, or to prevent them from having to plead the fifth about the charity in front of a jury and be subject to any inferences based on such a pleading, likely both. Neither, the filing says, is sufficient reason to keep this information from the jury.

The filing continues, Krawatsky seeks damages for lost income, earnings, emotional distress, specifically financial distress, but the availability of third party funds is relevant to asses the extent to which the Krawatskys actually experienced financial distress as a result of the families’ allegations.

The filing further argues that the Krawatskys are seeking damages that just don’t exist since the evidence shows that their income actually increased after the allegations against Shmuel Krawatsky were made, and was further supplemented by the ICF. Finally, the filing argues, the creation and existence of the ICF, them receiving funding monthly from the ICF, and the fact that they did not report the funds they received on their personal income taxes (according to the same deposition referenced above), are al indicative of their penchant for dishonesty, going to their credibility, which is admissible in a defamation case.

Any prejudicial effect testimony about the ICF may have on the jury, the filing argues, is a prejudice of the Krawatsky’s own making. They cannot have it both ways, the filing argues, insetting up and benefitting from a fraudulent charity that they failed to report, and then turning around and claiming that talking about such a fraud would be prejudicial toward a jury.